Airport Capacity Analyst, Christakis Christodoulou, looks at ACL’s initial coordination data for Summer 2022 and what this can tell us about the season ahead.

It goes without saying that Covid-19’s impact on the aviation sector has been significant. UK coordinated airports saw an average reduction of 70% in operated flights compared with pre-pandemic levels. Now, as Airport Coordination Limited (ACL) commence the coordination cycle for Summer 2022, we can start to get a view of airline demand in relation to initial submissions before coordination. Some might expect demand to be lower than pre-covid, as aircraft are removed from fleets, crew compliments reduced and consumer travel remaining uncertain. The story is not the case at all airports. Increased demand at this stage can be for many reasons including genuine incremental growth, positioning to exploit opportunities or uncertainty about recovery and future travel restrictions.

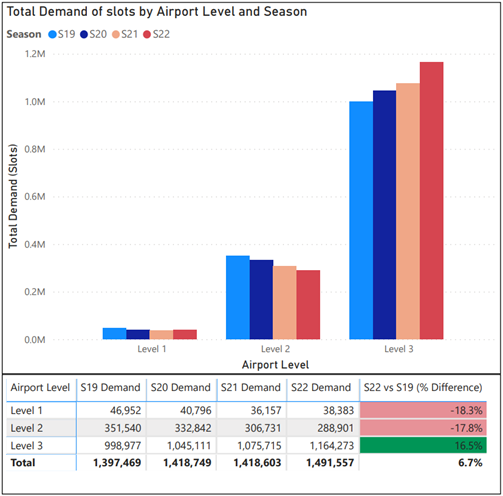

The graph below paints a picture of this divergence. Demand is reduced at Level 1 (data collection) and Level 2 (facilitated) airports, but increases significantly for larger, Level 3 (fully coordinated) airports. Demand activity decreased annually by an average of +7.9% (20,880 movements) at Level 2 airports, while simultaneously increasing by an average of +5.2% (55,099 movements) annually at Level 3 airports. This could be due to the less formal process at facilitated airports and the available capacity and/or lower competition for slots, making permissions easier to obtain as the coordination cycle progresses. Taking all ACL airports, Summer 22 demand has increased by +6.7% (94,088 slots) compared to Summer 2019.

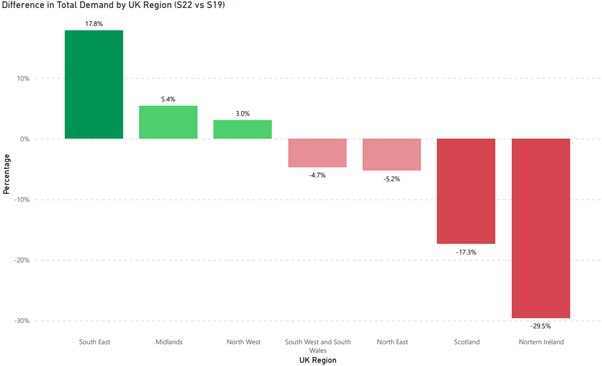

The following graph compares this difference at a regional level, comparing Summer 22 and Summer 19 demand by UK regions.

The South East, which has the highest concentration of Level 3 airports, saw the highest growth. Whereas Northern Ireland saw the greatest reduction. Only time will tell if this is a true reflection on what will materialise. ACL would expect, as the coordination cycle progresses, demand will level up as schedules become finalised.

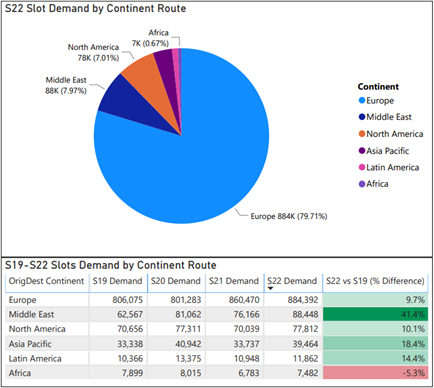

Initial data of the destinations intended to be served shows the UK and Europe accounting for 80% of Level 3 airport slot requests. Comparatively, Africa is the only continent to see a decrease in demand compared to Summer 19 season. While destinations in the Middle East saw the greatest growth in demand.

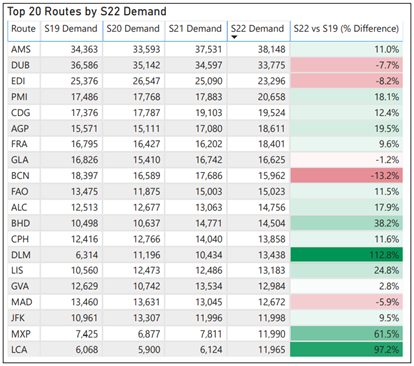

Further analysis identifies which routes are gaining popularity. The table below shows the top 20 destinations demanded during the Summer 22 initial coordination process across all UK Level 3 airports. Mallorca (PMI), Charles De Gaulle (CDG) and Malaga (AGP) are some of the many international routes experiencing an increase in demand. Amsterdam (AMS) is currently the most popular route across the Level 3 airports, facing an increase of 11% compared to pre-pandemic demand.

How accurate are these assessments?

Based on previous seasons, the data quality of initial demand data can vary and depend very much by airport. Demand for some airports tends to be genuine. Conversely, other airports are prone to receiving high demand which eventually falls away.

Demand can fall for various reasons. The coordinator may not be able to give the required time and so the slot becomes unfeasible for the operation. Or the airline may not get the slot at the other end of the route and so cannot complete the operation.

Market demand can also play a role in the eventual services operated. Airlines may seek to improve flexibility by requesting slots to build a pool to choose from as markets change. Similarly, requests may be made to test availability, with operational decisions made at a later stage. This is often common practice when airlines look to enter new markets and there are multiple options for airports in their chosen destinations.

All these examples are permitted under the slot process and with the uncertainty caused by Covid there are probably increased reasons for doing so.

Such high demand may also be misinterpreted. At a time when alleviation for Summer 2022 is still in discussions, many could conclude high demand negates a need for pandemic-related alleviation. Alternatively, it is equally uncertain whether demand at this stage is a product of ongoing uncertainty, justifying alleviation at a market-by-market level.

To answer the question, all data has its merits and a vast majority of demand data will be accurate. There will be a requirement to sensitise the data for planning purposes as history shows not everything planned will materialise and likewise services not currently planned will appear in the schedule. Those using data for planning purposes should be wary of drawing conclusions from a single snapshot. Nonetheless, ACL would urge carriers to return slots they do not intend to operate at the earliest opportunity so they can be reallocated as required by the WASG. Doing so gives airlines on the wait list greater opportunity to gain access or improve schedule optimisation and allows airports to better plan for the season ahead.